April 2026 ICE Mortgage Monitor

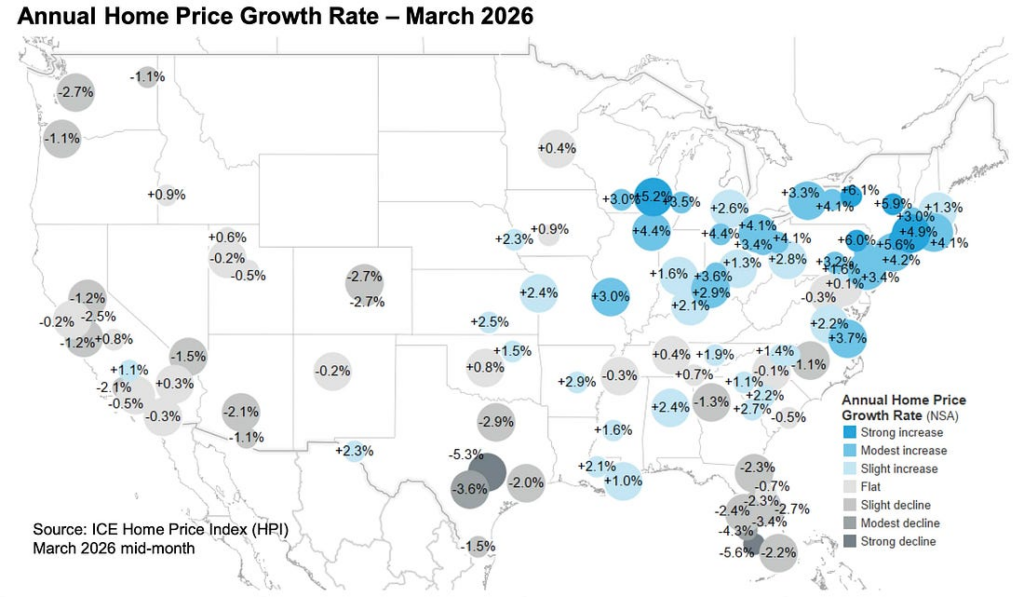

The April 2026 ICE Mortgage Monitor paints a housing market that is no longer in broad decline, but instead splitting into clear winners and losers. While national home price growth has slowed to near zero, the underlying story is far more nuanced. Some regions are seeing steady appreciation and tightening conditions, while others—particularly former boom markets—are still correcting.

This shift is critical for investors and buyers alike, as the market transitions from a post-pandemic correction phase into what appears to be an early-stage recovery.

A Clear Divide: Midwest and Northeast Lead the Market

The strongest home price appreciation in 2026 is concentrated in the Midwest and Northeast. These regions now dominate the list of top-performing housing markets, driven by a combination of limited inventory and improved affordability relative to prior years.

Cities such as New Haven, Syracuse, Scranton, and Albany are posting some of the highest year-over-year gains, with appreciation ranging from roughly 5% to over 7%. What makes these markets particularly notable is that they are benefiting from structural supply constraints. Inventory in many Northeastern markets remains significantly below pre-pandemic levels, which continues to support upward price pressure.

Unlike the pandemic-era boom markets, these areas did not experience extreme price inflation earlier in the cycle. As a result, they are now seeing more stable, sustainable growth rather than volatile swings.

Signs of Stabilization Nationwide

Although headline appreciation remains muted—national home price growth is just 0.4% year over year—the broader market is showing clear signs of stabilization.

Monthly price trends have improved significantly. Nearly 80% of markets are now experiencing positive or firming price momentum, a sharp reversal from last summer when the majority of markets were declining. The share of markets with monthly price drops has fallen below 20%, indicating that the correction phase is largely behind us in many areas.

This shift suggests the market is no longer deteriorating broadly. Instead, it is transitioning into a more balanced environment where local fundamentals—especially supply—play a much larger role.

Single-Family Homes Continue to Outperform

Another important trend is the divergence between property types. Single-family homes continue to outperform, with modest year-over-year gains, while condo prices are declining across many markets.

This reflects ongoing buyer preferences for space, privacy, and flexibility, as well as higher HOA costs and insurance pressures in condo-heavy regions. In fact, a majority of markets are now seeing falling condo prices, making this segment structurally weaker in the current cycle.

For investors, this reinforces the idea that not all real estate is equal. Asset selection matters more than ever.

The Weakest Markets: Florida, Texas, and the Mountain West

On the other side of the equation, the weakest housing markets are concentrated in the South and West. A total of 39 of the 100 largest U.S. markets are still experiencing year-over-year price declines, and nearly all of them fall within these regions.

Florida stands out as a major area of softness. Markets such as Cape Coral, North Port, Tampa, Orlando, and Jacksonville are all seeing declining prices, with some experiencing drops of more than 5%. Texas is also under pressure, particularly in Austin and San Antonio, where prices have fallen significantly from their pandemic peaks.

The Mountain West and parts of the broader West Coast are also struggling. Cities like Seattle, Denver, and Colorado Springs are still posting annual declines, even as monthly trends begin to stabilize.

Oversupply Is the Key Driver of Declines

The primary factor behind these declining markets is not demand collapse, but oversupply.

Many of the weakest markets today were the strongest during the pandemic housing boom. In response to rapid price increases, these areas saw a surge in new construction and listings. As demand cooled due to higher interest rates, inventory began to accumulate.

In some cases, inventory levels are now dramatically above pre-pandemic norms. Colorado Springs, for example, has nearly double its typical inventory, while Austin, Seattle, and several Florida markets also have substantial surpluses.

This excess supply is putting downward pressure on prices and giving buyers more negotiating power. It is also extending the correction cycle in these regions compared to supply-constrained markets in the Northeast.

A Market in Transition, Not in Crisis

Despite the weakness in certain regions, the broader housing market is not in distress. Instead, it is undergoing a gradual rebalancing.

Price declines are becoming less widespread, and even in markets with negative year-over-year numbers, monthly trends are beginning to stabilize. This suggests that many of these areas are approaching the end of their correction phase.

At the same time, stronger markets are seeing continued appreciation, supported by tight inventory and improving affordability conditions earlier in the year.

What This Means Going Forward

The most important takeaway from the April 2026 data is that real estate is now a highly localized investment. National trends matter less than regional supply and demand dynamics.

Markets with constrained inventory—particularly in the Midwest and Northeast—are likely to continue appreciating in the near term. Meanwhile, markets with significant inventory surpluses, especially in Florida, Texas, and parts of the West, may continue to face price pressure before fully stabilizing.

For investors, this environment presents both risks and opportunities. Oversupplied markets may offer attractive entry points, but they also carry the risk of further short-term declines. Conversely, tighter markets may provide more stable appreciation, albeit often with lower cash flow potential.

Ultimately, the housing market is no longer moving in one direction. It is fragmenting, and success will depend on understanding which side of that divide a given market falls on.